Social Security Benefits Outside the U.S.: When you think about retiring and living life to the fullest, the question of whether you can collect Social Security benefits outside the U.S. often comes up — especially if you’re dreaming of spending your golden years in a beach town in Mexico, sipping espresso in Italy, or visiting grandkids in Australia. The good news is that yes, most U.S. citizens who qualify for Social Security can still receive their monthly checks while living abroad — but there are some important rules, restrictions, and opportunities you need to understand before you decide where to call home. Social Security isn’t some abstract government program. It’s your money that you earned by working and paying Social Security taxes during your career. Because of that, you deserve clear, practical information that’s easy to follow, backed by official sources, and helpful for planning your future — whether you’re a retiree, a financial planner, or someone just curious about how this works.

Table of Contents

Social Security Benefits Outside the U.S.

Living abroad and collecting your U.S. Social Security benefits is not only possible — it’s common. But it requires planning. From understanding country rules and direct deposit options to Medicare limitations, tax planning, and currency considerations — each piece matters. With the right plan, your twilight years can be filled with adventure, comfort, and peace of mind — no matter where you choose to live.

| Topic | Details & Stats |

|---|---|

| Eligibility Abroad | Most U.S. citizens can receive Social Security outside the U.S. |

| Country Restrictions | Some countries (e.g., Cuba, North Korea) have restrictions |

| Direct Deposit | SSA direct deposit available in many countries |

| Noncitizen Rules | Benefits may stop after 6 months outside U.S. for noncitizens |

| Work Credits | Typically need ~10 years of work (40 credits) |

| SSI Benefits | SSI stops after 30 days abroad |

Understanding the Basics – What Social Security Is and Why It Matters

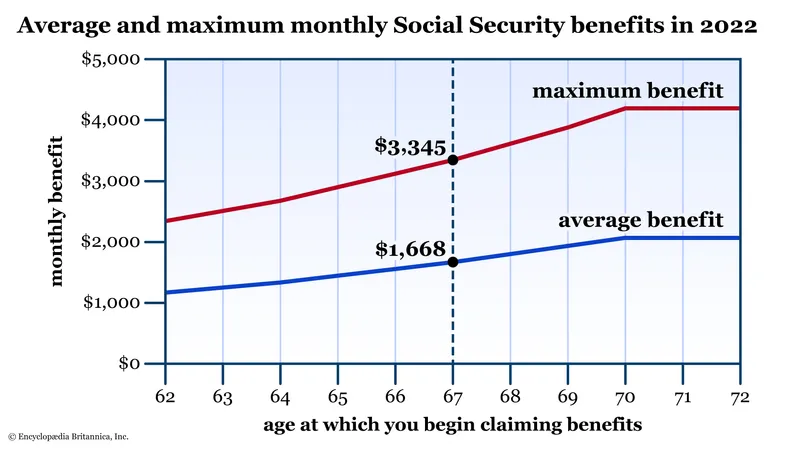

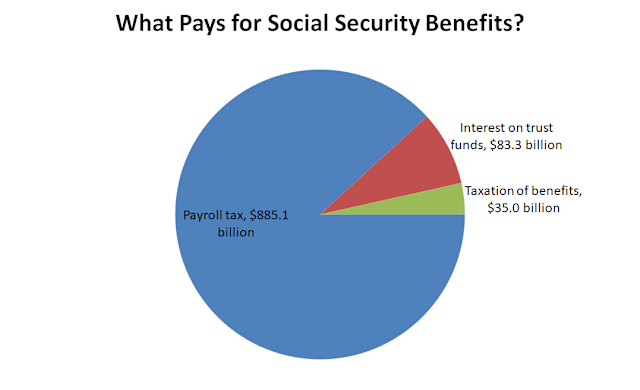

Social Security is a federal program that pays monthly benefits to retired workers, disabled individuals, survivors of deceased workers, and certain family members of beneficiaries. Most people become eligible for retirement benefits by earning work credits — typically, 40 credits, which is about 10 years of work in jobs covered by Social Security. You earn these credits by paying Social Security taxes through payroll deductions during your working years. USA.gov explains how eligibility works and maintains up‑to‑date guidance for people living overseas.

What’s essential to understand is that Social Security retirement and disability benefits are generally available outside the U.S., but Supplemental Security Income (SSI) — a needs‑based benefit — is not payable once you are outside the U.S. for more than 30 days.

Citizens vs. Noncitizens – Who Can Get Social Security Benefits Outside the U.S.?

U.S. Citizens and Nationals

If you’re a U.S. citizen or national who meets the eligibility requirements, you can usually receive your Social Security benefits while living in most countries overseas. There is no time limit on how long you can be outside the U.S. and still get paid, but your benefits may be restricted or held in a few specific countries that the Social Security Administration (SSA) lists as restricted (such as Cuba and North Korea). For most countries around the world, your benefit can continue month after month.

The SSA maintains a Payments Abroad Screening Tool that lets you check whether your benefits will continue in any specific country. This tool is updated regularly and is the official source for this type of information.

Non‑U.S. Citizens

If you are not a U.S. citizen, the rules are stricter. Generally, benefits will stop if you are outside the U.S. for six continuous months unless you fall under an exception. These exceptions can include temporary work assignments, totalization agreements (which we’ll talk about soon), or specific visa statuses. That’s why your status and how long you plan to stay outside the U.S. matter a lot in planning.

Country‑Specific Rules – Where Benefits Continue and Where They Don’t

The SSA provides a set of country lists that show whether payments continue indefinitely, have restrictions, or are not payable. For instance, if you plan to retire in Canada, France, Germany, Japan, or the U.K., those countries are typically on lists where benefits continue without major issues for U.S. citizens. On the other hand, benefits generally cannot be sent to countries such as Cuba and North Korea, and in those cases, benefits are held until you relocate to a place where payments are permitted.

How to Set Up Your Social Security Benefits Before Moving Abroad?

Here’s a practical, easy‑to‑follow guide to make sure your benefits are in place before you make the move:

1. Check Your Destination Country With SSA

Before you choose where to retire, use the SSA’s country screening tool to check whether benefits will continue in that country and under what conditions. This step alone can save weeks of confusion later.

2. Apply for Benefits Early

You can file for Social Security benefits up to four months before you want your payments to start, and you can do this while you’re still in the U.S. If you’ve already moved abroad, you can often apply through a U.S. Embassy or Consulate.

3. Set Up Direct Deposit

The SSA can deposit benefits directly into many foreign bank accounts. This eliminates the risk of lost or delayed checks and makes managing your finances overseas much easier. The SSA maintains a list of countries and banks that accept direct deposit

4. Keep Your Address and Contact Info Updated

Once you move overseas, make sure SSA always has your current address, phone number, and preferred mailing address. The SSA periodically sends questionnaires to verify your status — answer them promptly to avoid payment interruptions.

5. Report Life Changes Promptly

Major life events — like marriage, divorce, death of a spouse, or a move — can affect your benefits. Notify SSA right away to keep your benefit amount correct and avoid overpayments.

Medicare and Healthcare While Living Abroad

Here’s something that trips up a lot of retirees: Medicare usually does not cover healthcare services outside the United States.

That means if you retire to another country and rely on Medicare Part A and Part B for healthcare, you’ll likely need to purchase local or international health insurance once you’re abroad. Some countries have excellent public healthcare systems (like Spain, France, or Japan), but you may need to enroll in that system or buy supplemental coverage.

Taxes on Social Security Benefits When Living Abroad

Just because you live overseas doesn’t mean you escape U.S. tax obligations. U.S. citizens and resident aliens must still file annual U.S. tax returns and may owe tax on their Social Security benefits depending on their total income. Additionally, some countries tax Social Security income differently. That’s why it’s essential to consult a tax professional who understands expat tax law to avoid double taxation.

Currency, Cost of Living, and Financial Planning

When you’re receiving U.S. Social Security benefits in another country, your monthly check will be converted to local currency. That sounds simple, but exchange rate fluctuations can make a big difference in your actual spending power. If the dollar weakens, your benefits might not go as far against local prices; if it strengthens, your benefits can stretch further.

Also consider the cost of living in your destination country. Some places — especially in Southeast Asia or Central America — might be significantly cheaper than major U.S. cities, while others — like major European capitals — might be more expensive.

Work with a financial planner to model your budget based on local costs, healthcare expenses, taxes, and exchange rate risks.

Estate Planning and Your Social Security Abroad

If you plan to leave assets to heirs, own property overseas, or have beneficiaries in multiple countries, estate planning becomes even more important. Make sure your wills, power of attorney, and beneficiary designations comply with both U.S. and foreign laws. Work with attorneys in both jurisdictions to avoid probate complications.

Real‑World Examples

Imagine Joan and Luis, a retired couple. They both worked in the U.S. for decades and earned enough credits for full Social Security retirement benefits. They decide to retire to Portugal. Because Portugal is on the SSA’s list of countries that accept benefits, they continue to receive direct deposit monthly into a Portuguese bank account. They also enroll in private health insurance since Medicare doesn’t cover care in Portugal.

Now imagine Sara, who is a dual citizen — U.S. and Canadian. She moves to Canada and collects Social Security. Because of a totalization agreement, Sara can count some of her Canadian work toward U.S. Social Security eligibility, which boosts her benefit amount.

Pros & Cons of Collecting Social Security Benefits Outside the U.S.

Pros

- Potentially lower cost of living

- Cultural experiences and lifestyle changes

- Direct deposit available in many countries

- Possibility of combining work credits with totalization agreements

Cons

- Medicare usually does not cover healthcare abroad

- SSI benefits stop after 30 days outside the U.S.

- Some countries restrict SSA payments

- Possible tax complexities and exchange rate risks

Big changes are coming to Social Security in 2026: 5 important updates

Social Security 2026: How Much You Must Earn to Get the Highest Benefit

Working While Receiving Social Security – 2026 Rule Changes That May Affect Monthly Payments