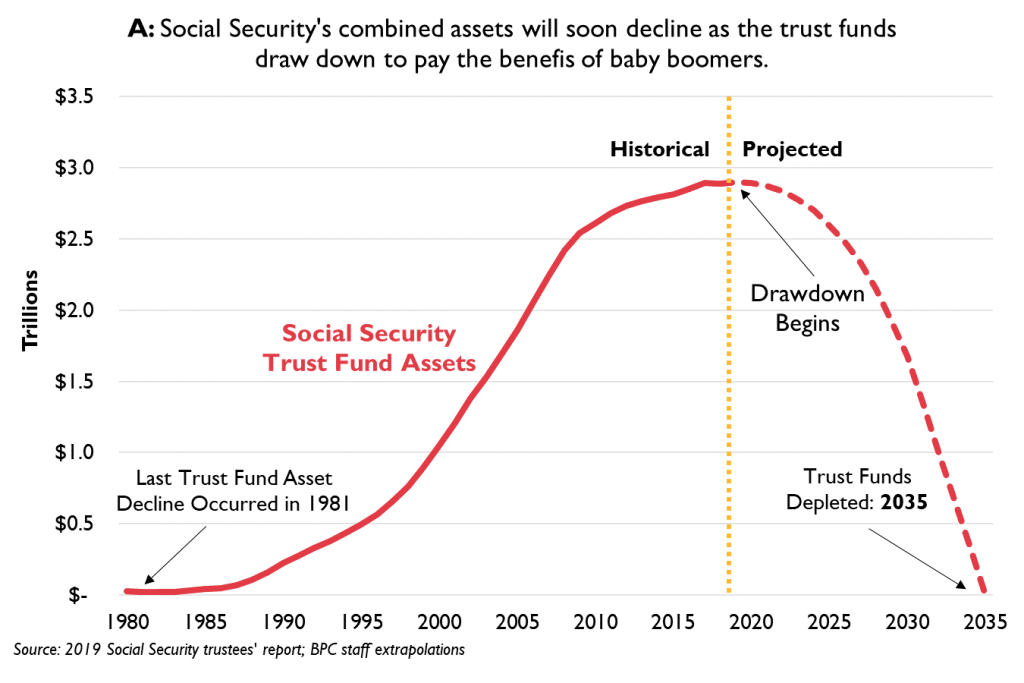

Social Security Benefit Cut Alert: If you’re banking on Social Security benefits to keep your lights on and food on the table during retirement, it’s time for a serious gut check. There’s a storm brewing that could lead to a $460 per month reduction in Social Security payments by 2033, affecting over 70 million Americans. This isn’t fearmongering—it’s a wake-up call. The writing is on the wall, coming directly from the Social Security Administration’s 2023 Trustees Report. While nothing is set in stone yet, the projections are loud and clear. If Congress doesn’t act, we’re headed straight for a 23% cut in benefits.

Table of Contents

Social Security Benefit Cut Alert

The projected Social Security benefit cut of $460 per month isn’t inevitable—but it’s a very real possibility if Congress doesn’t intervene before 2033. This looming reduction, affecting tens of millions of Americans, is a serious call to action. Your best defense? Get informed, prepare your finances, and advocate for policy changes. The longer we wait, the harder it gets. As financial literacy instructor Alex Beene wisely said:

“Hope for the best, prepare for the worst. Don’t rely entirely on that monthly check.”

| Topic | Details |

|---|---|

| Monthly Benefit Cut | Estimated $460 reduction per recipient |

| Date of Impact | Projected for 2033 if no reforms |

| Cause | Trust Fund depletion and rising retiree-to-worker ratio |

| Affected Groups | Retirees, disabled (SSDI), and survivor beneficiaries |

| Projected Payouts | Only 77% of scheduled benefits payable |

| Official Source | SSA Trustees Report 2023 |

Why Social Security Benefit Cut Alert?

To understand the risk, we need to look at how Social Security is structured. The system is a pay-as-you-go model. That means today’s workers pay FICA payroll taxes (6.2% from employees and 6.2% from employers) to fund current retirees. The money isn’t being saved for you in an account—it’s being used right now.

But the balance between payers and recipients has been thrown off. Here’s why:

1. Aging Baby Boomers

More than 10,000 baby boomers retire every day. That’s millions more people collecting benefits, which strains the system.

2. Fewer Workers Supporting More Retirees

In 2000, there were about 3.4 workers for every retiree. By 2035, there will be just 2.3 workers per beneficiary. That’s not enough to sustain current payout levels.

3. Longer Lifespans

Americans are living longer, and that’s a good thing—but it also means people draw Social Security for decades, not just years.

4. Shrinking Birth Rates

The U.S. birth rate has dropped below replacement level. Fewer babies today means fewer workers in the future paying into the system.

The Social Security Benefit Cut Alert: How They Got That Number

The average Social Security benefit for a retired worker in 2024 is approximately $1,907 per month. A 23% cut (based on the 77% payout projection post-trust fund depletion) equals roughly $438 less each month.

Some estimates round that up to $460, assuming cost-of-living adjustments (COLAs) continue annually.

So, the impact would look something like this:

- Current Benefit: $2,000/month

- Post-Cut Benefit: $1,540/month

- Loss: $460/month or $5,520/year

For someone on a fixed income, that’s devastating.

The Official Warnings: This Isn’t New

The Social Security Board of Trustees has issued annual warnings for years. In their 2023 report, they stated:

“If no legislative action is taken, the combined OASI and DI trust funds will become depleted in 2034, at which point continuing income will be sufficient to pay 80% of scheduled benefits.”

Will Congress Let This Happen?

Here’s the rub: No politician wants to be responsible for cutting grandma’s check.

But kicking the can down the road is risky. Every year of delay makes the fix harder. Solutions proposed over the years include:

- Raising the retirement age (gradually to 68 or 70)

- Lifting the taxable income cap (currently $168,600 in 2024)

- Adjusting benefit formulas for higher earners

- Increasing payroll taxes modestly across the board

Why Haven’t They Acted Yet?

Gridlock. Polarization. Election fears.

Legislation like the Social Security 2100 Act has been proposed but stalled. Lawmakers fear voter backlash or can’t agree on whether to raise taxes or cut spending.

What Social Security Benefit Cut Alert Means for Retirees and Pre-Retirees?

Now that we know what’s coming, what do we do about it?

Here’s your step-by-step guide to protect your future.

Step 1: Know Your Numbers

Visit SSA.gov/myaccount to get your projected benefits. This tells you what you’re currently eligible for based on your work history.

Then run a “what-if” scenario by reducing it by 23%.

Step 2: Delay Benefits If Possible

Every year you delay benefits past full retirement age (up to 70), your monthly check increases by 8%. This can offset future cuts—especially if you expect to live a long life.

Step 3: Diversify Your Retirement Income

Social Security should be one leg of a three-legged stool:

- Social Security

- Personal savings (IRA, 401(k), Roth IRA)

- Pensions or annuities (if applicable)

Build up the other legs now. If you’re in your 40s or 50s, ramp up contributions while you still can.

Step 4: Consider Part-Time Work in Retirement

Even just 10–15 hours a week can help plug the gap if your benefits are cut. And bonus: working can improve your mental health, social engagement, and delay full cognitive decline.

Step 5: Re-Evaluate Your Budget

Practice living on 75% of your projected benefits today—just to see how it feels. If it’s tight, look at ways to:

- Downsize your home

- Move to a lower-cost area

- Cut discretionary expenses

Real-Life Example: Fred and Maria’s Story

Fred (67) and Maria (66) retired in 2022. They each receive $1,800 in Social Security, totaling $3,600 monthly. They live in a modest home in Oregon and have $200,000 in retirement savings.

They’ve already started adjusting their spending to prepare for possible cuts in 2033. Their plan:

- Pay off their mortgage by 2029

- Delay drawing from their IRA until RMDs kick in

- Consider part-time consulting work post-70

Common Myths Debunked

Let’s clear up some confusion:

Myth: Social Security is going bankrupt

Fact: It’s not. The system will still bring in money from payroll taxes. It just won’t be enough to pay full benefits.

Myth: Only new retirees will be affected

Fact: If cuts happen, everyone—current and future recipients—may be affected.

Myth: The government will never let this happen

Fact: There’s no automatic fix. If Congress doesn’t act, cuts happen by law.

What Financial Planners Recommend

We reached out to several certified financial planners (CFPs). Here’s what they advise:

- Start saving 15% of your income today, no matter your age

- Delay Social Security if you’re in good health

- Consider Roth conversions to hedge against future tax hikes

- Invest conservatively but steadily in index funds

- Have a backup plan for long-term care and inflation

2027 Social Security COLA – Early Forecast Signals a Smaller Raise Than Expected

Which States Tax Social Security Benefits? Check the Full Map and What You Might Pay in 2026!

Social Security Boost by State 2026 – Five States Where Benefits Could Rise by Up to $2,000