Social Security and Medicare 2026: What Retirees and Savers Should Prepare for Now is one of the most important financial topics facing Americans this year. Whether you’re already retired, close to retirement, or just building your nest egg, understanding what’s changing in these vital programs is key to smart financial planning. With cost-of-living increases, rising healthcare premiums, shifting tax thresholds, and long-term funding concerns, it’s never been more critical to stay ahead. This article breaks everything down in plain English—no fluff, just facts—with clear examples and expert guidance to help you navigate the road ahead.

Table of Contents

Social Security and Medicare 2026

In 2026, Social Security and Medicare bring both opportunities and challenges. Benefits are going up—but so are healthcare costs. Retirement savings options are more flexible, but also more complex. And the long-term sustainability of these programs remains uncertain. What retirees and savers should prepare for now is proactive planning. Know your benefits, optimize your choices, and build a diversified retirement income plan. Take advantage of rising contribution limits, monitor your Medicare coverage annually, and delay Social Security if you can afford to. Stay informed, stay flexible, and take control of your retirement future.

| Topic | 2026 Update | Key Stat/Figure |

|---|---|---|

| Social Security COLA | Increased | +2.8% (~$56/month for average retiree) |

| Medicare Part B Premium | Higher | $202.90/month (standard rate) |

| Medicare Part B Deductible | Increased | $283/year |

| Social Security Wage Cap | Higher | $184,500 taxable wage cap |

| Medicare Advantage | More popular, fewer perks | 67% of enrollees have $0 premium MA plans |

| Retirement Law | SECURE 2.0 Changes | Higher catch-up contributions and RMD age changes |

| Trust Fund Solvency | Projected shortfalls by 2033 | Social Security may only pay ~77% of benefits |

Social Security in 2026 – What to Know

Cost-of-Living Adjustment (COLA)

Starting January 2026, Social Security benefits are going up by 2.8%. That’s the official COLA—the annual cost-of-living adjustment calculated based on inflation trends. For the average retired worker, that equals about $56 more per month or nearly $670 extra per year.

But here’s the catch: most retirees won’t feel the full bump because Medicare Part B premiums are also increasing, and they’re automatically deducted from your Social Security check. So while the gross check may rise, the net amount you receive could be modestly higher—or nearly flat.

This COLA affects nearly 71 million Americans, including retirees, disabled workers, and Supplemental Security Income (SSI) recipients.

Full Retirement Age (FRA)

If you were born in 1960 or later, your full retirement age is 67. This matters because:

- Claiming Social Security at 62 means a permanent reduction in benefits (up to 30% less).

- Waiting until 70 means you’ll get delayed retirement credits that increase your benefit by about 8% per year past FRA.

This strategy—known as delayed claiming—can substantially improve lifetime retirement income, especially for those who expect to live into their 80s or beyond.

Taxable Wage Base

The maximum taxable earnings subject to Social Security tax in 2026 is now $184,500 (up from $176,200 in 2025). If you’re a high earner, more of your income will be taxed (at 6.2% for employees or 12.4% if self-employed), although your potential future benefit will also rise slightly.

Medicare in 2026 – Breaking Down the Changes

Medicare provides health insurance to Americans 65+ and certain disabled individuals. But it’s not free, and in 2026, costs are rising across the board.

Part A – Hospital Insurance

For most people, Part A is premium-free. But for those who haven’t worked enough quarters (or spouses who don’t qualify through their partner), the premium for Part A can go as high as $505/month in 2026.

The hospital deductible under Part A also increases to $1,736 per benefit period. This covers the first 60 days of a hospital stay.

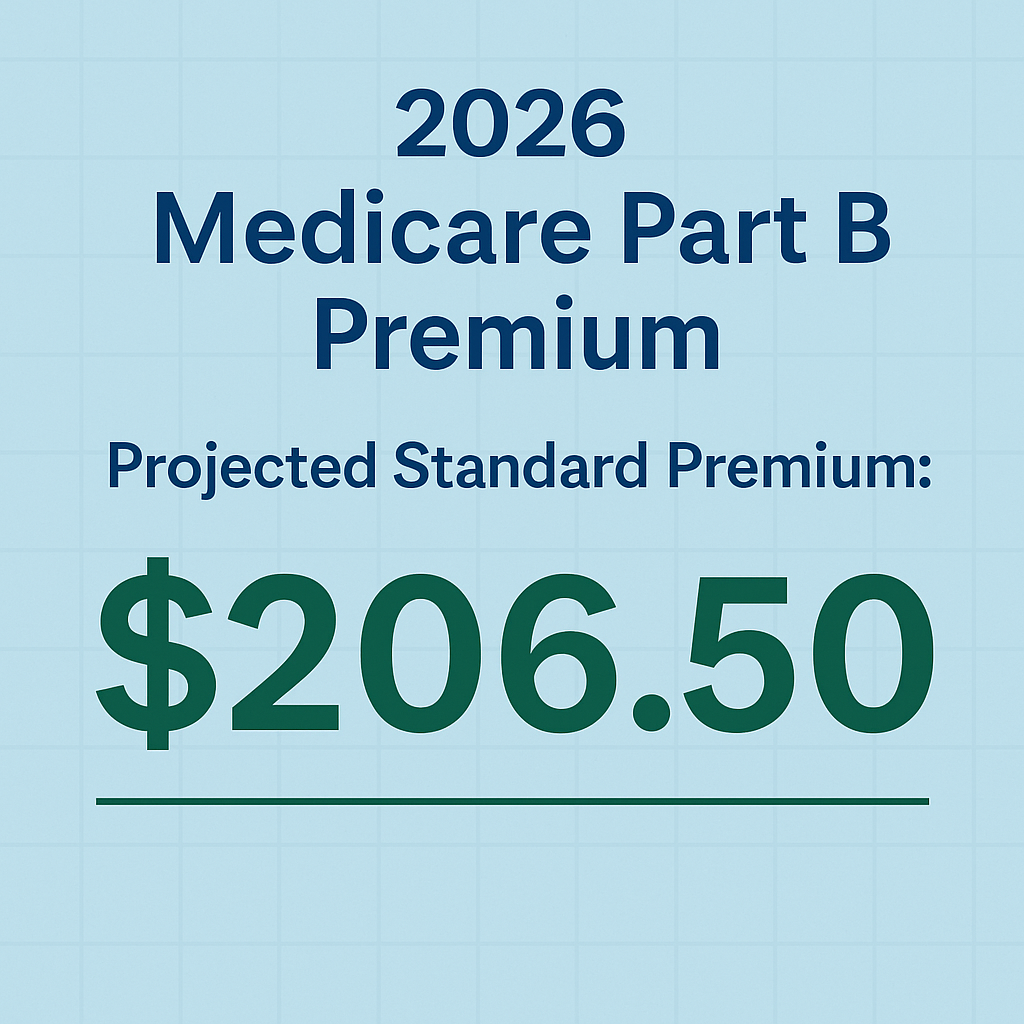

Part B – Outpatient Care

This is where most retirees feel the pinch.

- Monthly premium: $202.90 (standard)

- Annual deductible: $283

For higher-income individuals (above $103,000 for single filers), Income-Related Monthly Adjustment Amounts (IRMAA) apply, meaning you’ll pay more for Part B and Part D.

Part D – Prescription Drug Coverage

Thanks to the Inflation Reduction Act, 2026 brings out-of-pocket caps on prescription costs:

- Annual limit on Part D spending: ~$2,000

- Insulin: Still capped at $35/month

- Vaccines: Now free under Part D

This is huge for seniors with chronic conditions requiring expensive medications.

Medicare Advantage and Medigap in 2026

More than 30 million Americans now choose Medicare Advantage (MA) plans instead of traditional Medicare. In 2026:

- 67% of MA plans have $0 additional premiums beyond Part B.

- However, fewer plans offer fringe benefits like gym memberships or free meals compared to 2025.

- MA plans often limit doctor networks, unlike Medigap + Original Medicare which allows more flexibility.

Choosing between MA and Medigap is a personal decision. Consider:

- Your budget

- Your doctors’ network participation

- Your prescription drug needs

Open enrollment for MA and drug plans runs every year from October 15 to December 7.

Trust Fund Warnings – Why You Should Still Plan Ahead

The Social Security Trust Fund that pays retirement benefits is projected to be depleted by 2033, according to the 2023 Trustee Report. If Congress does nothing, Social Security would only be able to pay about 77% of promised benefits after that.

Medicare’s Hospital Insurance (Part A) trust fund faces a similar shortfall around 2031.

This doesn’t mean the programs will disappear—but it does mean future benefit cuts or tax increases are likely if no legislative changes are made.

What you should do:

- Don’t rely on Social Security alone.

- Plan for other income sources (401(k), IRAs, HSAs, pensions, rental income, etc.).

- Be flexible with your retirement age and budget.

Retirement Savings Rules and SECURE 2.0 Act

The SECURE 2.0 Act, passed in late 2022, continues to roll out changes in 2026 that can benefit savers.

Here’s what’s new:

- Required Minimum Distribution (RMD) age is now 73 (rising to 75 in 2033).

- Catch-up contributions: If you’re aged 60–63, you can contribute even more to 401(k)s.

- Automatic 401(k) enrollment: New workplace plans must automatically enroll employees (though they can opt out).

- Saver’s Match: Low- and moderate-income workers receive government matches into their retirement accounts (starting 2027, but you can prepare now).

Take advantage of these opportunities by:

- Maxing out contributions: In 2026, 401(k) limits rise to at least $24,500, plus $7,500 catch-up for those 50+.

- Using HSAs: Health Savings Accounts offer triple-tax benefits and can be used for retirement healthcare.

Practical Steps to Take for Social Security and Medicare 2026

Here’s a simple checklist:

1. Review your Social Security Statement

- Log in to ssa.gov and check your benefit estimates.

2. Compare Medicare plans

- Use the Medicare Plan Finder to compare drug and Advantage plans.

3. Consider delaying Social Security

- Waiting until 70 can significantly boost lifetime income.

4. Increase your retirement savings

- Use employer plans, IRAs, HSAs, and Roth accounts.

5. Watch your income

- Avoid IRMAA penalties on Medicare by managing taxable income in retirement.

6. Talk to a financial planner

- A pro can help you coordinate Social Security, Medicare, and tax strategies.

Social Security Benefit Boost 2026 – 3 Simple Moves That Can Increase Your Monthly Check

Social Security 2026: How Much You Must Earn to Get the Highest Benefit

Working While Collecting Social Security 2026 – The Earnings Limit That Keeps Your Benefits Safe