Average Social Security Payments: If you’ve ever asked yourself, “Am I getting more or less than the average Social Security payment?” you’re not alone. Whether you’re a retiree enjoying your golden years, a professional planning ahead, or someone helping aging parents make smart decisions, this topic matters. And it matters big time because Social Security isn’t just a check — it’s a central piece of most Americans’ retirement income. In this friendly, expert‑level guide, we’ll break it all down in plain English — no fluff, no confusing jargon, no mystery. By the end, you’ll understand where your benefit stands compared to the national average, how it’s calculated, why it changes with age, and what you can do about it.

Table of Contents

Average Social Security Payments

So are you getting more or less than the average Social Security payment? The quick answer: If your monthly benefit is above ~$2,071 (as of 2026 for retired workers), you’re above average. If it’s below that, you’re under the average — but that’s just a benchmark, not a final verdict on your financial future. What matters most is knowing your benefit, understanding how it’s calculated, comparing it to averages, and planning smartly with your retirement goals in mind. Social Security is a powerful piece of your financial puzzle — and now you have the insight to make it work in your favor.

| Category | Stat / Info | Source |

|---|---|---|

| 2026 Average Monthly Benefit (Retired Worker) | ~$2,071 per month | Social Security Administration (SSA) |

| Cost‑of‑Living Adjustment (2026 COLA) | +2.8% increase (~$56/mo for average beneficiaries) | SSA official COLA page |

| Full Retirement Age | ~67 (for most people born 1960 or later) | SSA Benefits Info |

| Maximum Possible Monthly Benefit | ~$4,000 to $5,400+ (depending on earnings and age claimed) | SSA Maximum Benefit Tables |

| Years Used to Calculate Benefits | Highest 35 years of earnings | SSA Benefit Calculation |

What Exactly Is the Average Social Security Payments

When people talk about the average Social Security check, they usually mean the average for retired workers, not all beneficiaries like disabled, survivors, and spouses.

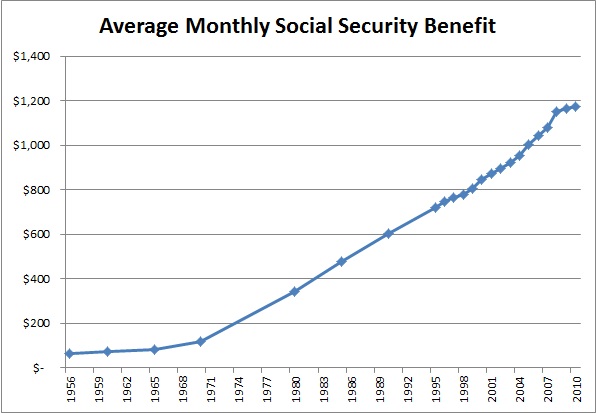

According to the Social Security Administration (SSA), in 2026 the average monthly benefit for retired workers is about $2,071. This number comes straight from SSA estimates and reflects all retired workers receiving Social Security benefits as of the latest reporting period.

Here’s an important point: this is not a guaranteed benefit for everyone — it’s simply the average across all retired workers currently drawing checks.

A slightly lower overall average (around $1,865 to $1,900) appears in some retirement planning reports that include all benefit types (disabled, survivors, etc.). But if you’re focused on retirement income, the $2,000‑plus figure is the most useful comparison.

How Social Security Benefits Are Calculated: The Basics

Understanding the average number won’t help much unless you know how your benefit is figured.

Here’s the step‑by‑step way Social Security calculates your benefit:

Step 1 — Track Your 35 Highest‑Earning Years

Social Security reviews your earnings history — the wages you paid Social Security taxes on — and selects the 35 years with the highest earnings.

If you don’t have 35 years of earnings, Social Security fills in the gaps with zeros, which will lower your average.

Step 2 — Index Your Earnings for Inflation

The SSA adjusts your wages for inflation — older dollars are “bumped up” to reflect current wage levels so that lifetime earnings are fairly compared.

Step 3 — Compute the Average Indexed Monthly Earnings (AIME)

SSA averages your indexed earnings over 35 years and divides by 12 to arrive at your AIME. This is the base number used in benefit formulas.

Step 4 — Apply the Primary Insurance Amount (PIA) Formula

With AIME calculated, SSA applies a formula with “bend points” (different percentages for different portions of your AIME) to compute your Primary Insurance Amount (PIA) — the core amount you’d receive if you claimed at your full retirement age.

Step 5 — Adjust for Claiming Age

This is crucial. If you start benefits before your Full Retirement Age (FRA), your benefit is reduced permanently. If you delay claiming past FRA — up to age 70 — your benefit grows thanks to delayed retirement credits.

Why Your Benefit Might Be More Than Average Social Security Payments?

So you’ve got a Social Security check above ~$2,071 per month — nice! That could happen for several reasons:

High Lifetime Earnings

If you consistently earned at or above the Social Security wage base — and paid Social Security taxes on those earnings — your benefit will be higher.

For example, someone who made high wages for most of their career might have a PIA well above average.

Delayed Claiming

If you wait to claim Social Security until age 70, your benefit can increase roughly 8% per year after your Full Retirement Age, thanks to delayed retirement credits.

So even if someone had average earnings, delaying claiming until age 70 can push their check above average.

Strategic Claiming Tactics

Couples can sometimes boost total lifetime benefits by coordinating claiming — for example, one spouse claiming earlier while the higher‑earning spouse delays.

Why Some People Get Less Than Average Social Security Payments?

Not great if your check is smaller than average? Don’t worry — here are common reasons why that happens:

Claiming Early

If you claim at age 62 — the earliest age allowed — Social Security permanently reduces your benefit. For many, that reduction can be up to 30% compared to what you’d get at FRA.

Lower Lifetime Earnings

If your career involved part‑time work, gaps (for caregiving or education), or years of low earnings, your AIME will be lower — and so will your benefit.

Missing Years

If you didn’t work at all for a period of time, zeros are factored into your 35‑year average — which pulls the overall number down.

Evaluating Your Personalized Social Security Benefit

Now that you understand averages, here’s how to find your personal number and see how it compares:

Step 1 — Create or Sign In to My Social Security

Go to SSA’s official site and create a my Social Security account:

https://www.ssa.gov/myaccount/

This gives you access to your verified earnings history and benefit estimates.

Step 2 — Review Your Earnings Record

Make sure your earnings are accurate. Any missing wages should be corrected with the SSA to ensure your benefit is calculated correctly.

Step 3 — Look at Benefit Estimates

SSA shows your monthly benefits at different claiming ages — e.g., age 62, FRA, and age 70.

Write those numbers down — that’s your personal Social Security picture.

Step 4 — Compare to Averages

Now you can see:

- If your benefit is above average

- Within an average range

- Or below average

Remember averages are guidelines — what matters is how your benefit fits into your overall retirement plan.

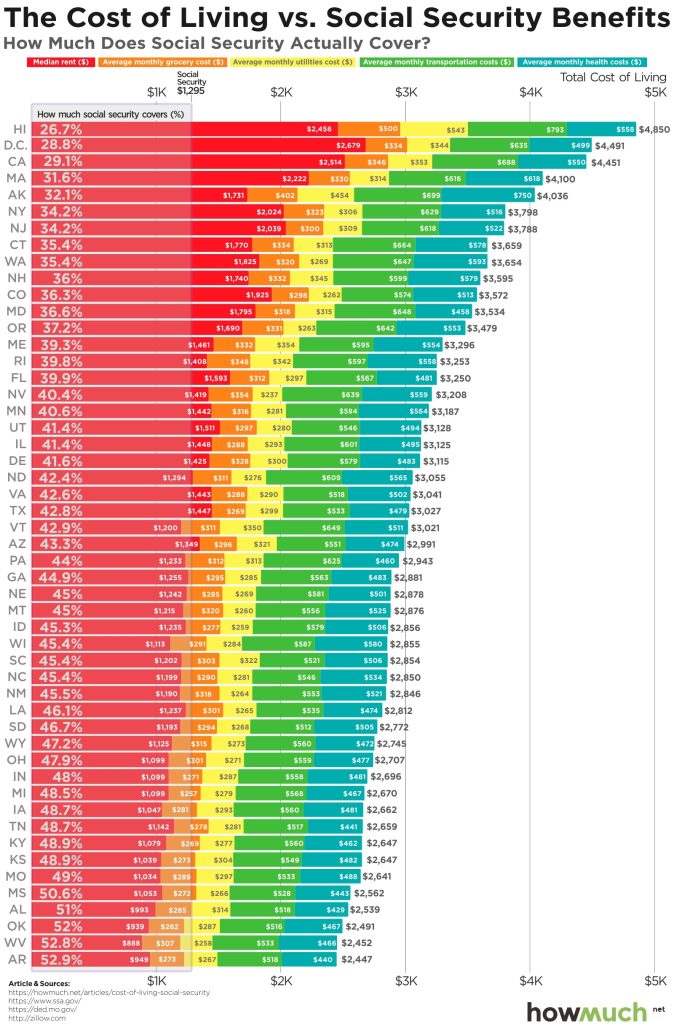

How Medicare and Health Costs Affect Your Benefit?

Social Security ties into other retirement systems — most notably Medicare.

Even though Medicare premiums are technically separate from Social Security benefits, many people see their Medicare Part B and Part D premiums automatically deducted from their monthly check. That means the net amount you actually spend could be less than the gross benefit.

That’s important to consider when you compare your benefit to the average.

The Role of Taxes

Yes — Social Security benefits can be taxable, depending on your income:

- If your combined income (including retirement savings withdrawals, wages, etc.) exceeds certain levels, up to 85% of your Social Security benefits may be taxable at the federal level.

- Not all states tax Social Security, but a few do.

So your take‑home amount can differ significantly from your gross check.

Pro Strategies to Maximize Social Security Income

Here are practical ways to think strategically about your Social Security:

Delay Claiming When Possible

Delaying from FRA to age 70 boosts your monthly check — sometimes by tens of thousands of dollars over time.

Coordinate With Spouse

Married couples can use claiming tactics to maximize total household benefits — such as filing and suspending or survivor benefit timing.

Account for Taxes

Plan distributions (IRAs, 401(k)s, etc.) to manage taxable income — which can reduce taxes on your benefit.

Factor in Inflation Adjustments

SSA applies a Cost‑Of‑Living Adjustment (COLA) each year. In 2026, the COLA was +2.8%, meaning the average benefit increased by roughly $56 a month.

Keeping track of COLA helps ensure your spending power doesn’t erode over time.

Real‑World Case Studies

Here are two simplified examples that show how claiming age affects benefits:

Case A — Early Claimer: Jane claims at age 62. Because she claimed early, her benefit is permanently reduced — maybe around $1,600/mo even though the average is ~$2,071.

Case B — Late Claimer: Sam waits until age 70. Even with average earnings, his benefit might be $2,600 or more.

These aren’t guaranteed amounts — but they show how timing and strategy matter.

Common Mistakes to Avoid

Here are some pitfalls that can hurt your benefit or your retirement income picture:

- Claiming too early because you think you “need the money”

- Not reviewing your earnings history for accuracy

- Ignoring how Medicare premiums affect net benefits

- Forgetting that your spouse has benefits too

Planning ahead beats last‑minute decision making.

Social Security Abroad Rules – Countries Where Payments Are Restricted in 2026

Social Security Boost by State 2026 – Five States Where Benefits Could Rise by Up to $2,000

Average Social Security Benefits 2026 – New Monthly Payment Amounts by Retirement Age