Car Loan Tax Deduction: now that’s a headline making waves across the U.S., especially among car buyers, tax preparers, and anyone trying to stretch a dollar in 2025 and beyond. For the first time in decades, interest paid on personal car loans is deductible — no itemizing required, no business use needed. Let’s break it all down like a good neighbor would — so it’s easy to follow, trustworthy, and packed with what you need to know whether you’re driving a brand‑new pickup or helping someone file taxes in a CPA’s office.

Table of Contents

Car Loan Tax Deduction

The New $10,000 Car Loan Tax Deduction is a rare chance for everyday drivers to get a tax break on one of life’s biggest (and most common) expenses. Whether you’re a young buyer trying to afford your first car, a growing family upgrading your wheels, or a taxpayer looking to legally lower your bill — this deduction is worth watching. Plan wisely, keep records, and work with a pro if needed — and you’ll be in the driver’s seat come tax time.

| Feature | Details |

|---|---|

| Deduction Amount | Up to $10,000 per year in car loan interest |

| Years Eligible | 2025, 2026, 2027, 2028 |

| Eligible Vehicles | New, U.S.‑assembled, under 14,000 lbs, personal use |

| Who Can Claim | U.S. taxpayers with qualifying loans |

| Loan Requirements | Must begin after Dec. 31, 2024; secured by vehicle |

| Filing Requirements | Standard or itemized filers — both qualify |

| Income Limits | Phases out at ~$100K (single) / ~$200K (married) MAGI |

| Official Source | IRS Car Loan Interest Deduction Guidance |

The Big Picture: Why Car Loan Tax Deduction Exists

Historically, interest on personal auto loans wasn’t tax deductible. Sure, if you were self-employed and using a car for business, you could deduct mileage or interest tied to that business use. But if you were just a regular family buying a new minivan? No dice.

That changed with the One Big Beautiful Bill Act, signed into law in 2025. It was part of a wider legislative package aimed at reducing household debt pressure, boosting domestic auto production, and making ownership more attainable as car prices and interest rates surged.

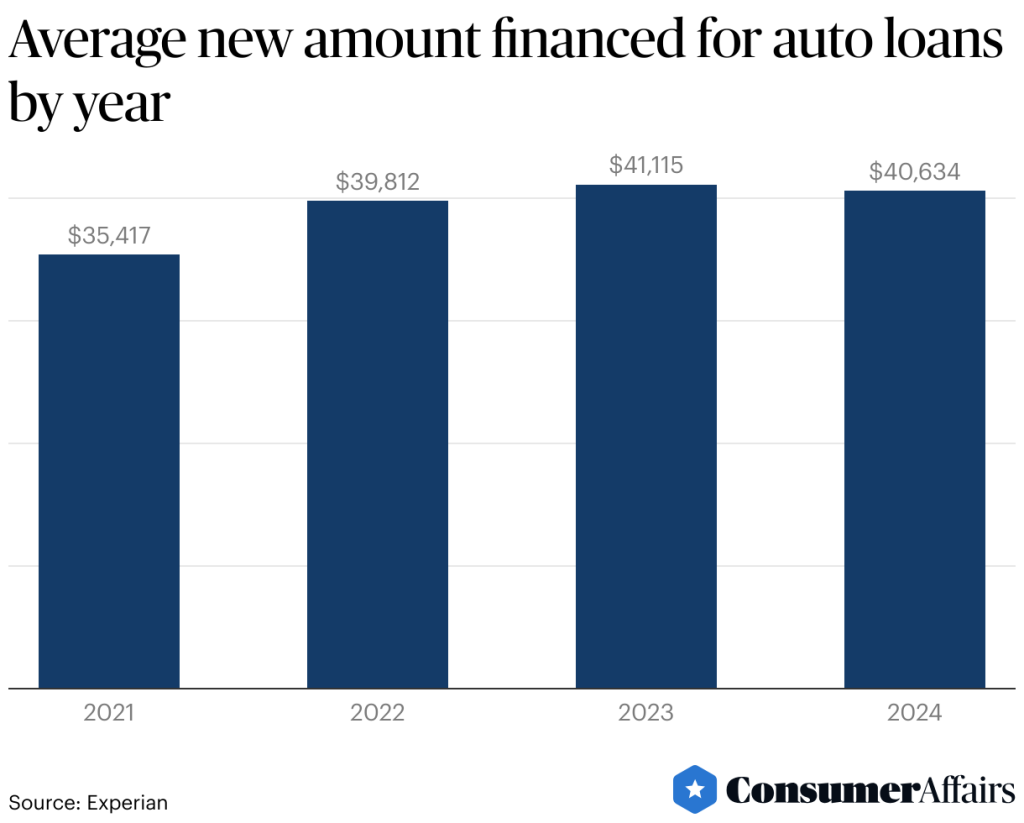

In fact, according to data from Kelley Blue Book and Edmunds, the average new car price in 2024 was over $48,000, and average interest rates for auto loans hovered around 7.1%. That means many buyers are shelling out thousands a year just in interest — money they used to eat with no tax benefit.

Now? A chunk of that cost is deductible, giving relief to millions.

Who Qualifies for the Car Loan Tax Deduction?

Not everyone qualifies — and that’s where a little planning goes a long way. Here’s who can claim this deduction, based on IRS guidelines:

You Must Be:

- A U.S. taxpayer with a valid Social Security number

- Filing your return for tax year 2025 or later (up to 2028)

- Paying interest on a qualifying loan for a new car

Your Loan Must:

- Begin after December 31, 2024

- Be secured by the vehicle

- Be used solely to buy the qualifying car

Your Car Must Be:

- New — not leased or used

- For personal use (not business-exclusive)

- Assembled in the U.S.

- A passenger vehicle under 14,000 lbs — includes sedans, SUVs, pickup trucks, minivans, and motorcycles

Income Limits:

This isn’t a tax break for the ultra-rich. The deduction begins to phase out for:

- Single filers over $100,000 MAGI

- Married filers over $200,000 MAGI

If you’re over the limit, you’ll still get a partial benefit up to a certain cutoff (usually ~$150K single / ~$250K joint).

How to Claim the Car Loan Tax Deduction (Step-by-Step Guide)?

- Finance a Qualifying Car After Dec. 31, 2024

- Ensure it’s a new, U.S.-assembled, personal-use vehicle

- Keep the loan documentation, dealer invoice, and VIN records

- Track Interest Paid

- Your lender may issue a statement similar to a Form 1098 (mortgage interest) showing the interest paid in a tax year

- Alternatively, you may need to calculate this from your amortization schedule

- File with IRS Form 1040

- The IRS will likely introduce or revise a schedule (such as Schedule 1 or a new Schedule 1-A) for the deduction

- Include the car’s VIN when claiming

- Retain All Records

- In case of audit, keep:

- Sales invoice

- Financing documents

- Loan payment records

- Proof of U.S. assembly (typically on the Monroney sticker or via VIN decoder)

- In case of audit, keep:

Real-Life Examples: See It In Action

Example 1: First-Time Buyer

Maria, 24, buys a new U.S.-assembled Toyota Corolla in January 2025 for $26,000. She finances it at 6.5% interest over 6 years. In 2025, she pays around $1,980 in interest.

- Her income is $52,000 — well below the phaseout

- She claims the full $1,980 deduction

- That could lower her federal tax bill by $396, assuming a 20% effective tax rate

Example 2: Married Couple

Luis and Jasmine, married filing jointly, earn $205,000 MAGI in 2025. They finance a $70,000 electric truck and pay $6,800 in interest.

- They’re within the phaseout range, so their deduction is partially reduced

- Still, even a 50% deduction on that interest = $3,400 off their taxable income, saving them up to $680–$1,000 in taxes

Expert Tips to Maximize Your Car Loan Tax Deduction

- Buy Early in the Year

The sooner you buy, the more interest you’ll pay in the first year — maximizing your deduction potential. - Choose a Vehicle with U.S. Assembly

Not all Toyotas, Hondas, or Fords qualify — some are built overseas. Use the VIN decoder at nhtsa.gov to verify U.S. assembly. - Avoid Leases and Used Cars

No matter how sweet the deal, leased and used vehicles don’t qualify under the law. - Keep Your MAGI Low

Contribute to retirement accounts (like a 401(k) or Traditional IRA) to lower your Modified Adjusted Gross Income and stay within deduction limits.

Economic Impact: Why Congress Passed This Law

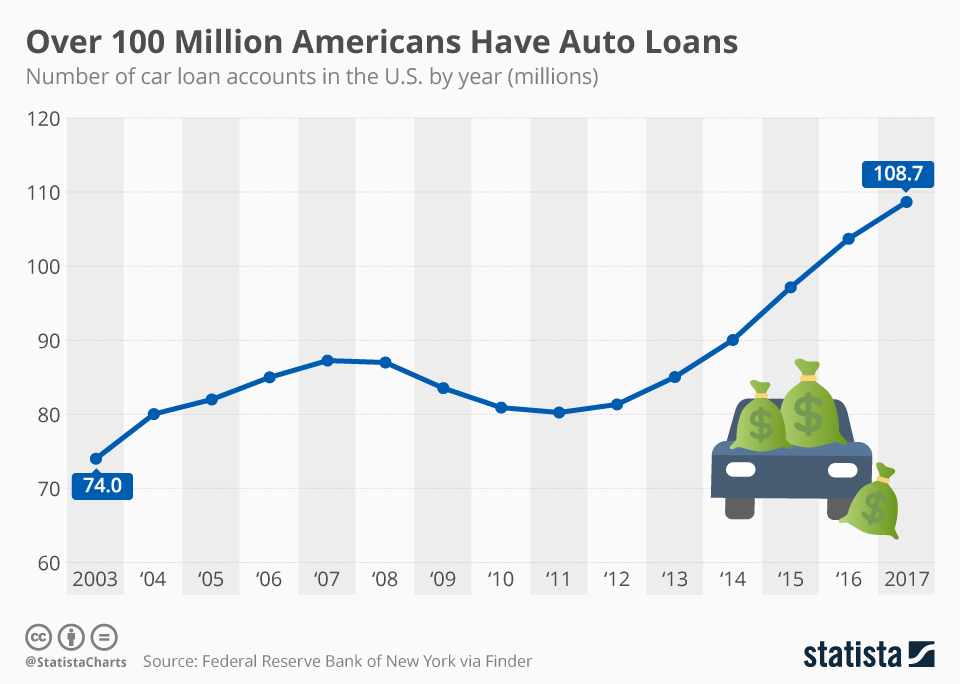

The U.S. auto market has changed dramatically over the last decade. The average new car loan term is now 72–84 months, and monthly payments often exceed $730.

Combine that with higher Federal Reserve interest rates, and you’ve got a generation of buyers drowning in interest — often paying more in finance charges than equity value in the first two years.

Congress introduced the deduction to:

- Encourage new car buying (boosting U.S. manufacturers)

- Relieve middle-income debt pressure

- Counteract declining auto affordability

It’s essentially a stimulus baked into the tax code — rewarding buyers for staying in the new car market while supporting American jobs in manufacturing.

How It Compares to Other Tax Deductions?

| Deduction Type | Max Amount | Itemizing Required? | Use Case |

|---|---|---|---|

| Car Loan Interest (New, 2025–28) | $10,000 | No | Personal new car loans |

| Mortgage Interest | Unlimited (up to loan cap) | Yes | Home loan |

| Student Loan Interest | $2,500 | No | Qualified student loans |

| Medical Expenses | Varies | Yes | Over 7.5% of AGI |

| Charitable Donations | Varies | Yes | Donations to 501(c)(3) |

The car loan deduction joins a rare group of “above-the-line” write-offs that don’t require itemizing. That makes it extra valuable for households that usually just take the standard deduction.

$1702 Stimulus Payment 2026: Is It Really Confirmed?

$1,000 Stimulus Checks for All – 2026 Full Payment Schedule for Seniors

IRS Tax Refund 2026 Schedule: Check Amount & Estimated Dates for Refund Payments