Social Security at Age 70: How Waiting Can Raise Your Monthly Benefit to $2,500 is a conversation that’s heating up around dinner tables, financial advisor offices, and on porches across America. And it should be — because this one decision can make or break how comfortably you live in retirement.

Whether you’re nearing retirement or planning ahead for the long game, waiting until age 70 to collect your Social Security retirement benefits can supercharge your monthly check. We’re talking about potentially earning $500 to $1,500 more per month, for the rest of your life. This article will walk you through everything you need to know — in plain English — with expert-backed tips, real-life examples, and a breakdown of the numbers.

Table of Contents

Social Security at Age 70

Waiting until age 70 to claim Social Security can be a retirement game-changer, adding thousands of dollars a year to your income for life. While it’s not the right move for everyone, those who can afford to wait often find it one of the smartest financial decisions they’ll ever make. It’s about more than just maximizing dollars — it’s about peace of mind, financial security, and giving yourself options in your golden years. If you’re serious about your retirement strategy, take the time to run the numbers, use the SSA tools, and talk to a trusted financial advisor.

| Topic | Details |

|---|---|

| Full Retirement Age (FRA) | Age 67 for most Americans (born in 1960 or later) |

| Earliest Claim Age | 62 (results in up to 30% reduction in benefits) |

| Delayed Retirement Credits | ~8% increase in benefits for every year delayed after FRA until age 70 |

| Maximum Monthly Benefit (2026) | $5,251/month for highest-earning individuals who wait until age 70 |

| Average Monthly Benefit (2026) | Approximately $2,071/month for all retired workers |

| No Additional Increases After 70 | Benefits cap out at age 70 — no further increases |

| Official Resource | Social Security Administration |

What Is Social Security and How Does It Work?

Social Security is a federal program designed to provide you with a monthly income after retirement. You earn the right to Social Security benefits by working and paying payroll taxes (FICA) for at least 10 years, or 40 quarters.

The amount you receive in retirement is based on your highest 35 years of earnings. If you didn’t work for 35 years, zeros are averaged in, which lowers your benefit. So, more years at a higher income = bigger check.

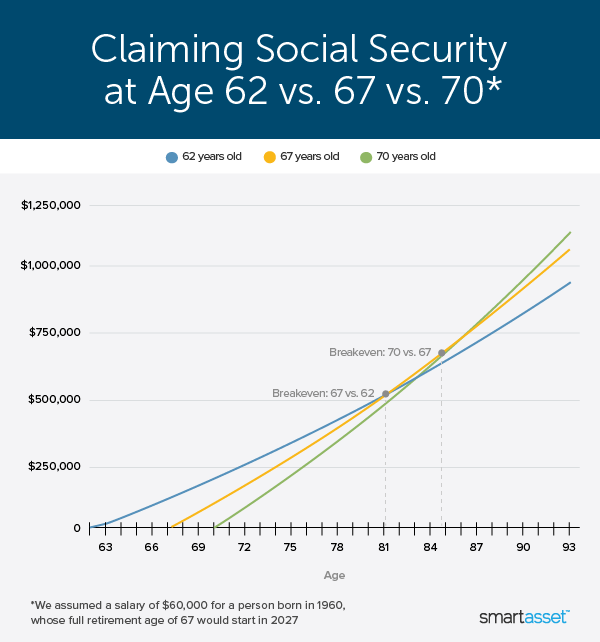

Claiming Ages: What Are Your Options?

Age 62: The Early Bird

You’re eligible to start benefits at age 62 — but it comes with a catch. You’ll receive permanently reduced benefits — up to 30% less than you would at Full Retirement Age.

For example, if you’re supposed to get $2,000/month at age 67, starting at 62 would only net you around $1,400/month.

This might be okay if you need the money urgently or have health concerns that affect longevity, but you’ll be locking in a smaller check for life.

Age 67: Full Retirement Age

This is the standard age when you receive 100% of your calculated benefit. No penalty, no bonus. It’s the “base level.”

If your Full Retirement Benefit (also called your Primary Insurance Amount or PIA) is $2,000, this is what you get at age 67.

Age 70: The Power Play

Waiting until age 70 means you’ll earn delayed retirement credits — about 8% extra for each year you wait past your FRA. That means by age 70, you’ll be receiving 124% of your benefit.

If your FRA benefit is $2,000, that bumps up to around $2,480/month — a $480/month increase for life, not counting future cost-of-living adjustments (COLAs).

How Much More Can You Earn by Waiting?

Let’s compare monthly payouts based on claiming age for someone whose FRA benefit is $2,000:

| Claim Age | Monthly Benefit |

|---|---|

| 62 | ~$1,400 |

| 67 | $2,000 |

| 70 | ~$2,480 |

Now multiply that by 12 months, and you’re looking at an extra $9,600/year just by waiting from age 67 to 70.

If you live into your 80s or 90s — and statistically, many Americans do — that extra income can really stack up.

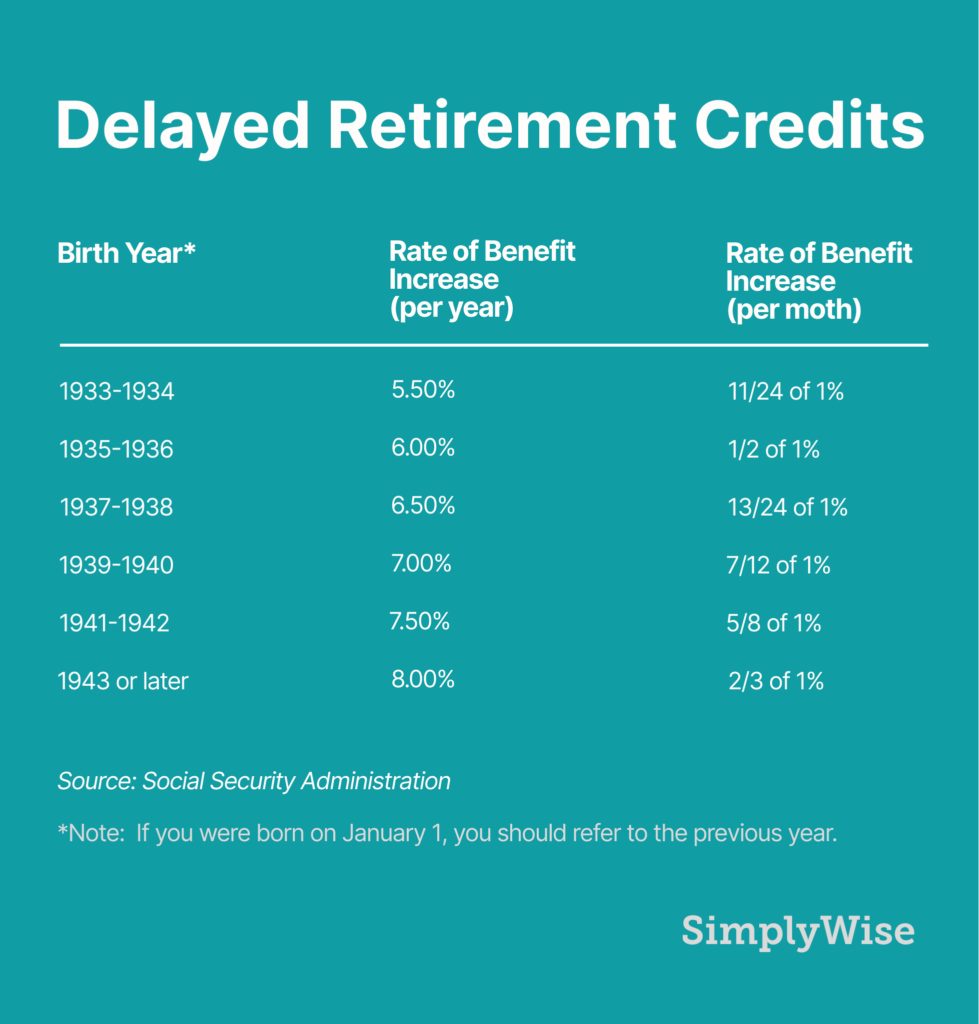

Understanding Delayed Retirement Credits

The Social Security Administration rewards patience. For every month you delay past your FRA, your benefit increases by about two-thirds of 1%, or roughly 8% per year.

- 1 year delay = 8% more

- 3 year delay (from 67 to 70) = 24% more

- Increases stop at age 70

This makes Social Security one of the only guaranteed income streams that grows the longer you wait — with no market risk involved.

Social Security at Age 70: Real-Life Case Studies

John: Moderate-Income Earner

- Career: 40 years as a warehouse manager

- FRA benefit: $1,800/month

- At age 70: $2,232/month

Extra per year: $5,184

Extra over 20 years: $103,680

Maria: High-Income Professional

- Career: 35 years as an executive

- FRA benefit: $3,800/month

- At age 70: $5,251/month

Extra per year: $17,412

Extra over 20 years: $348,240

That’s a life-changing difference.

When Should You Delay Social Security at Age 70?

Reasons to Wait:

- You’re in good health with a long life expectancy

- You have other income or savings to live on

- You want to maximize survivor benefits for your spouse

- You want inflation-protected income for the long haul

Reasons to Claim Early:

- You have a shorter life expectancy

- You need the income immediately

- You’re not working and have no other retirement funds

- You want to collect longer, even if it’s smaller

There’s no one-size-fits-all answer. A financial advisor can help tailor a strategy.

How Working After Age 62 Affects Benefits?

If you claim early and still work, earnings limits apply. For 2026, the annual limit is $22,320. Exceed that, and $1 is withheld for every $2 earned above the limit.

Once you reach FRA, you can earn as much as you want with no penalty. Plus, continued earnings may increase your future benefits if they replace lower-earning years in your 35-year average.

Spousal and Survivor Benefits

Waiting can benefit your spouse too.

If you pass away, your surviving spouse can receive your full benefit amount — so the higher it is, the better for them. This is especially important if your spouse earned less or didn’t work outside the home.

Tax Considerations

Your Social Security income may be taxed depending on your total income:

- Individual filers: If your combined income exceeds $25,000

- Joint filers: If combined income exceeds $32,000

Up to 85% of benefits can be taxed. It varies by state, too — some states like Colorado, Vermont, and New Mexico still tax benefits

Common Mistakes to Avoid

- Claiming too early out of fear

- Not checking your earnings record (mistakes = lower benefits)

- Forgetting survivor/spousal strategy

- Not considering taxes or healthcare costs

- Assuming Social Security will cover all expenses (it’s only meant to cover ~40% of pre-retirement income)

Social Security Changes 2026 – What Beneficiaries Need to Know Before Payments Update

Social Security Eligibility Income 2026 – The Exact Earnings Needed to Qualify

Social Security Maximum Benefit 2026 – Who Can Receive the $5,251 Monthly Check