Federal vs. Private Student Loans: Choosing between federal and private student loans in 2026 isn’t just about picking the cheapest option—it’s about setting yourself up for financial success after college. With tuition costs still climbing and student loan policies evolving, it’s critical to understand what you’re signing up for. Whether you’re a student, a parent, or returning to school later in life, this detailed guide is here to help you make a smart, confident decision.

Table of Contents

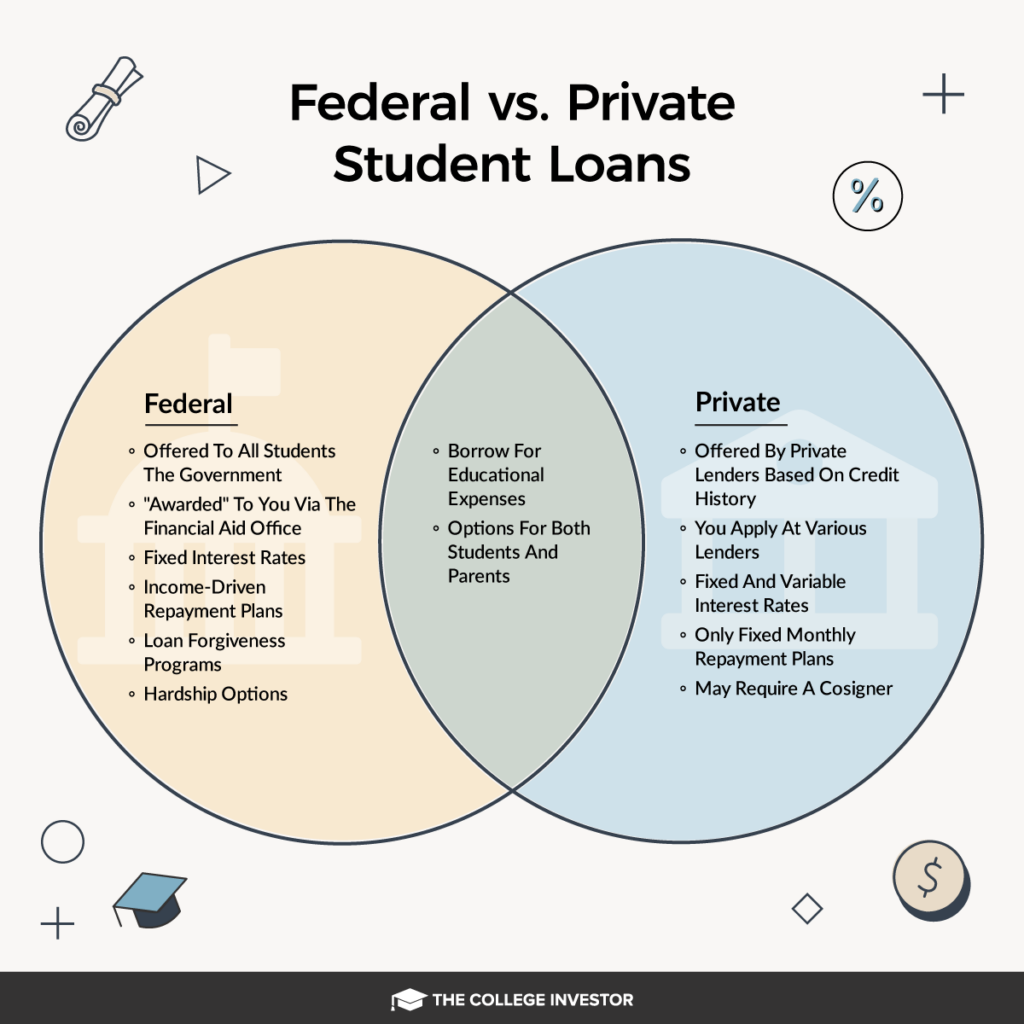

Federal vs. Private Student Loans

In 2026, the smartest move for most students is to start with federal student loans. They offer lower, fixed interest rates, built-in protections, and forgiveness options. Only consider private student loans if you’ve hit your federal borrowing limits and understand the repayment terms clearly. Don’t just chase money—chase the money that works for you long-term.

| Feature | Federal Student Loans (2026) | Private Student Loans |

|---|---|---|

| Lender | U.S. Department of Education (studentaid.gov) | Banks, credit unions, fintech lenders (e.g., Sallie Mae, SoFi, Earnest) |

| Interest Rates | Fixed: 5.50%–8.05% based on loan type | Variable or fixed: 5.99%–14.5% based on credit and cosigner |

| Credit Check | Not required (except PLUS loans) | Almost always required; rates depend on credit profile |

| Cosigner Requirement | Rarely needed | Often required, especially for undergraduates |

| Repayment Flexibility | Income-Driven Repayment (IDR), deferment, forbearance, forgiveness options | Limited options, varies by lender, often stricter repayment schedules |

| Forgiveness Programs | Yes — PSLF, IDR forgiveness, Teacher Loan Forgiveness, and others | No forgiveness programs offered |

| Borrowing Limits | Yes — Undergrads: $5,500–$12,500/year; Grads: up to $20,500/year | Can borrow up to cost of attendance, based on creditworthiness |

| Loan Origination Fees | Yes — around 1.057% to 4.228% (depends on loan type) | Varies — sometimes no fees, but higher interest rates may apply |

| Best For | Most students — especially those with low income or limited credit history | Students with strong credit, cosigners, or those needing to fill the federal loan gap |

Understanding Student Loans in 2026

Student loans, in simple terms, are borrowed money that must be paid back—with interest. But not all loans are the same. Federal loans are offered by the U.S. government with protections and limits, while private loans are issued by financial institutions and come with fewer safety nets.

Context: Rising College Costs in 2026

According to the latest data from the National Center for Education Statistics, the average annual cost for public four-year colleges in 2026 has climbed to over $26,000, including tuition, fees, room, and board. For private colleges, it’s closer to $45,000.

So, unless you’ve got that kind of cash saved up—or a full ride—you’ll likely need student loans.

Federal Student Loans: Safe, Predictable, Forgivable

Federal loans are often the first (and best) option for most students. Here’s why they’re so popular:

Types of Federal Loans Available

- Direct Subsidized Loans: For undergrads with financial need. Interest is paid by the government while you’re in school and during deferment.

- Direct Unsubsidized Loans: For undergrads and grad students. You’re responsible for the interest from day one.

- Direct PLUS Loans: For grad students or parents of undergrads. Requires a basic credit check.

Each loan has different limits and terms, but all federal loans are eligible for federal repayment plans and forgiveness options.

Benefits of Federal Loans

- Income-Driven Repayment (IDR): Payments adjust based on your income and family size.

- Forgiveness Programs: Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and others forgive remaining debt after 10–25 years of qualified payments.

- Deferment & Forbearance: Temporary pause on payments during hardship, illness, unemployment, or military service.

- No Cosigner Needed: Great for students with little or no credit history.

Private Student Loans: When Federal Isn’t Enough

Private loans fill in the gap when federal aid isn’t sufficient to cover your college costs.

Who Offers Private Loans?

- Banks (e.g., Wells Fargo, Citizens Bank)

- Online lenders (e.g., SoFi, Earnest, College Ave)

- Credit unions

Key Features (and Warnings)

- Credit-Based: Your interest rate is determined by your credit score. If you’re under 25, you’ll probably need a cosigner.

- Interest May Be Variable: This means it could start low but increase over time.

- Repayment Starts Sooner: Some lenders require payments while you’re still in school.

- No Forgiveness Options: You are fully responsible for repayment—even in tough circumstances.

When Private Loans Make Sense?

- You’ve maxed out federal loans

- You have excellent credit or a qualified cosigner

- You’re pursuing a high-paying field and want flexible terms

- You understand the risks and repayment requirements

Scholarships and Grants: Free Money First

Before borrowing anything—always hunt down free money.

- Apply for FAFSA to access federal grants like Pell Grants

- Use scholarship search platforms like Fastweb, Scholarships.com, and your state’s education department

- Check with tribal, religious, or professional organizations

- Ask your school’s financial aid office about institutional scholarships

Comparing Federal vs. Private Student Loans: Real-Life Scenario

Meet Elijah, a sophomore from Arizona with big dreams of becoming a civil engineer. His college costs $32,000/year.

- Federal Loans Awarded: $7,500

- Pell Grant: $6,895

- Scholarships: $5,000

- Total Need: $32,000 – $19,395 = $12,605

What Elijah Does:

- Accepts federal loans

- Applies for a private loan to cover the remaining $12,605

- Picks a lender offering fixed 7.2% interest with no in-school payments

Now, Elijah knows exactly what he owes, how long it will take to repay, and has a plan to refinance after graduation.

Federal vs. Private Student Loans: How to Apply for Student Loans in 2026

Step 1: Complete the FAFSA

Go to https://studentaid.gov and submit the Free Application for Federal Student Aid. This unlocks federal loans, grants, and school aid.

Step 2: Review Your Financial Aid Package

Each college will send an award letter showing how much you’re offered in grants, work-study, and loans.

Step 3: Accept Federal Loans First

Take what you need—don’t borrow more than necessary. Subsidized loans should be your top choice.

Step 4: Shop for Private Loans (if needed)

Use comparison tools like Credible, LendEdu, and individual bank offers. Look for:

- Fixed APR vs. Variable

- Cosigner release policies

- Flexible repayment

Step 5: Understand Your Repayment Terms

Know your grace period (usually 6 months post-graduation for federal loans), payment amounts, and how interest accrues.

Common Mistakes to Avoid

- Borrowing more than needed: Just because you’re approved doesn’t mean you should take the full amount.

- Ignoring interest: Interest starts ticking on unsubsidized and private loans right away.

- Not applying for scholarships: Every dollar you don’t borrow is a dollar you don’t have to repay—with interest.

- Defaulting on loans: Missing payments wrecks your credit and can lead to wage garnishment.

- Refinancing federal loans too soon: You lose forgiveness and flexible repayment options.

Student loan SAVE plan ending: how much could change your monthly payment?

First Time Repaying Student Loans? Essential Steps to Get Started Smoothly

House GOP’s New Health Plan Explained — And Why ACA Subsidies Aren’t Included